Contemplations on the Complicated Consequences of Joint Accounts

Joint ownership of financial assets, discussed as JTWROS (Joint Tenants with Right of Survivorship) in this article, is often viewed as a panacea for easily transferring assets to beneficiaries after death in a tax efficient way. Owning financial assets in joint name is a common technique used in estate planning. However, many may not fully grasp the complicated nature of joint accounts and the legal, tax and succession risks involved.

How can utilizing joint ownership help?

- Avoid probate or other estate administration taxes because the asset is transferred immediately upon death;

- Gives the joint owner(s) access and control of the assets in the event of incapacity;

- Prevents estate disputes because the asset automatically passes to the survivor.

While joint ownership can help in these ways, there are no guarantees joint ownership will achieve these objectives unless the intent and legal structure of joint ownership are clearly documented in such a way that it is defensible in a court setting.

The Burden of Proof

It is often assumed that, in Ontario and many other common law provinces, joint accounts come with a right of survivorship, meaning the surviving owner becomes the owner on death without the asset having to flow through the estate and be subject to probate.

In reality, due to precedent set in the Canadian Supreme Court by Pecore v. Pecore, there is an assumption that the surviving owner was simply holding the account in trust for the deceased’s estate and that there is a burden of proof on the surviving owner to rebut this assumption and there was a clear intent to transfer property at death. The need to prove intent has been reinforced time and time again in court in common-law jurisdictions.

Setting up joint accounts/assets is just the start!

If You Get It Right, What Are The Risks/Consequences?

Even if you get it right, and there is a clear intent to gift the assets when establishing a joint asset/account, there are a number of risks or unintended consequences, including:

- Deemed disposition and other negative tax effects – adding a joint owner often results in a deemed disposition (sale at fair market value for tax purposes). For non-registered assets, this can trigger capital gains tax, that in many cases, will surpass any savings related to probate. Joint ownership can still come with income attribution whereby the original sole owner shoulders all the taxable income generated by the joint asset(s).

- Loss of the capital gains exemption for personal real estate – in the case of real estate, joint ownership can also affect one’s, or one’s child’s ability to use the principal residence exemption to fully avoid paying capital gains tax on one’s home after joint ownership is established.

- Exposure to creditors and marital breakdowns of the joint owner – the jointly held assets can be pursued by creditors of the new joint owner, are subject to any claims arising from legal or financial problems, and can be included in any family property claims related to marital/relationship breakdown. Time brings change, some for the good and some for the bad, and sometimes the change is outside the control of the joint owner.

- Joint owner attains equal rights to the asset(s) – the new joint owner can withdraw or invest any joint assets without consent of the giver, any decisions regarding the joint asset may require their consent, and the form of joint ownership (e.g. tenants in common, joint tenancy) can be changed at any time. While best intentions and trust are almost always present when joint ownership is established, relationships and/or values can change over time, opening the door to disagreement and abuse of the joint asset in future.

And If You Get It Wrong?

If it is not 100% clear that establishing a joint asset/account was intended as a gift with a right of survivorship:

- The asset is deemed part of the estate – If the joint owner is unable to verify the intention of the joint account, courts may find that the asset remains part of the deceased’s estate, resulting in additional probate costs as well as opening the door to estate litigation.

Gift Letters and Establishing a Gift of Property

A gift letter, a deed of gift or a gift of beneficial right of ownership establishes a true gift and is necessary to prove intention. These documents should clearly state the intent as a transfer of ownership and be signed and dated by both parties. To avoid confusion and solidify intent, documenting why the joint asset is being established, how funds flow (into or out of the asset) and what happens in the event of incapacity or death. These documents can be established when the joint asset is established or even after the fact if the joint asset already exists.

Like all documents that may be subject to the scrutiny of the court, including witness signatures and/or legal representatives in the creation of the document can help improve the document’s validity and certify that all parties were present and had capacity at the time of signing.

Alternatively, even if a true gift is not the intention and the joint owner is expected to hold the funds in trust for the estate, this arrangement should be documented in writing and signed by both parties to confirm the joint owner’s agreement to act as trustee.

Are there alternatives to utilizing joint accounts?

Clarifying one’s goals and the intended outcome of establishing a joint account can help determine whether a joint account, or another option, is needed. Is the objective to:

- Ensure access to the asset/funds?

- Reduce/eliminate probate?

- Simplify intergenerational transfer?

Achieving some of these goals doesn’t necessarily require a joint asset/account. A well-drafted will, utilizing a trust, or establishing a power of attorney for property (POA) can be used for financial management of the asset(s) without transferring ownership, albeit with some exposure to probate. If the key objective of establishing a joint account/asset is access to the asset/funds or simplifying generational transfer, these options may be superior to a joint account/asset. If the goal is to reduce/eliminate probate, weighing the cost of probate relative to the capital gains taxes payable or exposure to risks above is crucial.

Because incorporating joint accounts/assets or similar structures involves coordinating legal, tax and securities matters, it is important to involve all three of your legal, tax and wealth management professionals in this planning.

If you have questions regarding joint accounts/assets, or other estate planning matters, feel free to reach out to us at Steele Wealth Management.

News and our views

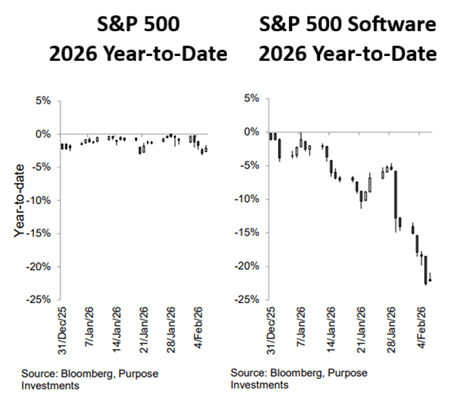

The ‘AI Scare Trade’ Re-Introduces Creative Destruction to Equity Markets. Since ChatGPT hit the scene in late 2022, the AI trade has been almost exclusively treated as a positive for large corporations whose stocks trade in public equity markets, and these markets have performed well since. The market consensus is that those companies providing the hardware and software to enable AI will clearly benefit but those companies that use AI to reduce headcount and improve profit margins will also be rewarded. This outlook strongly favours larger businesses that can invest in and quickly integrate AI to the detriment of smaller competitors that have fewer financial resources and potentially more antiquated business processes.

The idea that AI will be good for equity markets as a whole has been flipped on its head in 2026. Although the stock prices of certain companies have felt the looming pressure of AI for some time already – such as companies offering tools for website design, software development, or financial, legal, or other data analysis – new functionalities introduced by Anthropic’s Claude AI accelerated the decline in the above-mentioned sectors but also introduced concerns about how AI could negatively affect companies operating in previously unscathed sectors like logistics/transportation, insurance, real estate services and wealth management.

Our Take: Many stocks operating in the sectors noted above now trade at multi-year low valuations and could present opportunities if investors are wrong about the severity of the negative impact related to AI. In the short-term, the most likely course of events is that well-healed companies will utilize AI to cut jobs and boost efficiency and profit margins, and potentially gain a competitive edge relative to peers, supporting stock prices. Longer-term, especially as AI’s capabilities improve, it seems likely that a small number of individuals with strong industry knowledge could utilize AI to create new organizations to compete with, and potentially beat, larger companies that still have too much overhead for the post-AI world.

In logistics/transportation, an industry that is highly fragmented and includes thousands and thousands of independent operators, adoption of AI software that organizes pickups and drop-offs at a low cost could be incredibly rapid, disrupting larger companies currently providing a similar service to operators in the space. In industries where competition is much more concentrated or where the businesses require a human touch, adoption of AI software that allows existing or new entrants to become more efficient at a lower cost could be quite slow. Going forward, differentiating each industry’s ‘AI risk’ and ‘AI reward’ from an Economics 101 point of view may become increasingly important.

Either way, don’t expect incumbents to sit idly by as AI tries to take its share of the pie!

Just for fun

- No place like (almost) home! Filou, aka trickster, a French cat who went missing on a family vacation to Spain, traveled almost 250km across mountains, rivers and international borders back to his hometown. The funny part is that he didn’t go all the way home but instead hung out in the neighbourhood for weeks. Pretty tricky to travel 250km to just hang out a few hundred metres from home. As the old adage goes, home is where our neighbours feed us 😉

- Forbes 30 Under 30 or the FBI’s Most Wanted List for White-Collar Crime? Forbes 30 Under 30 is a set of lists published annually by Forbes magazine since 2011 that recognize 30 notable people under 30 years old in various industries. Dozens of individuals have been convicted of fraud and other crimes and/or embroiled controversy shortly after being named to the list. Forbes even admitted to its ability to identify future misfeasors with its own Hall of Shame, a list of 10 individuals in the 30 Under 30 it wishes to ‘walk back’. In 2023, one entrepreneur estimated that “the Forbes 30 Under 30 have collectively raised US$5.3 billion in funding… [and] have also been arrested for frauds and scams worth over US$18.5 billion”. Yikes! This month, another 30 Under 30 honoree was charged with fraud by US prosecutors, just two months after being named to the list.

![]()