Fourth Quarter 2025 : Sometimes It Pays to Gold with the Flow

Metals and Mining Stocks Push Equity Markets Higher in Q4 While Tech and AI Stocks Continue to Flounder

2025 finished the way it started – metals and mining stocks outperforming and big tech underperforming.

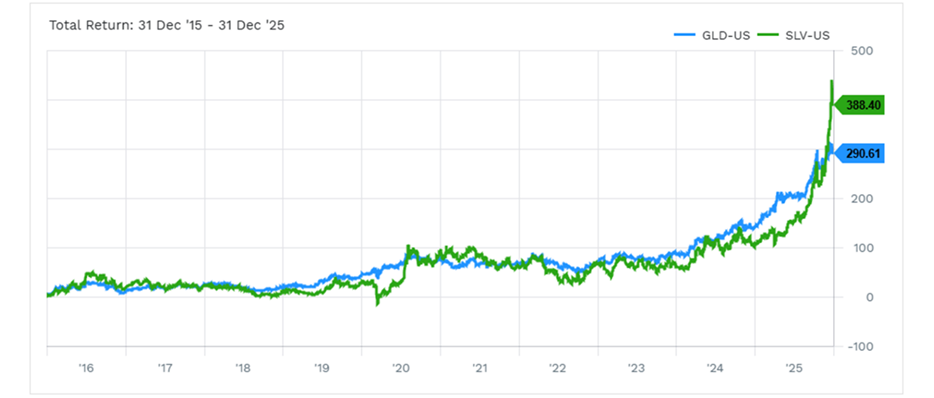

The TSX Material Sector, which represents metals and mining stocks in Canada and consists of ~80% gold and silver producers, rose 101% in 2025, well above the TSX Composite Index (Canada) at 32% (still excellent), the S&P 500 (US) at 18% (not too shabby) and the All-Country World Index at 22% (not too shabby either).

Investors had a number of reasons to gravitate toward the metals and mining sector in 2025, including:

- US President Trump’s executive orders to produce more critical minerals in North America (silver was added to the critical mineral list in late 2025) and his administration’s direct investment in a number of mineral development companies.

- A ~10% decline in the global US dollar index in 2025, making precious metals cheaper for foreign buyers and investors and pushing speculators away from US dollar investments and toward assets that help preserve capital like gold.

- An increase in industrial demand due to higher spending on AI chips and data centres which use gold, silver and other metals for reliable connectivity in critical areas.

- Historically significant government deficits that seem to grow with each passing year in nearly every country around the world and commitments to increase spending on defense (e.g. NATO members agreed to increase defense spending to 5% of GDP, from 2% currently, by 2035) that ensure deficits and potentially high inflation are here to stay.

- Relentless buying by global central banks as a store of value (e.g. the People’s Bank of China has bought gold every month for the past 14 months while central banks in Russia and Saudi Arabia have recently included silver in their precious metals portfolios).

- The ongoing war in Ukraine, continued tensions between Israel/US and Iran, and subsequent to year end, the capture and arrest of Venezuelan President Nicolas Maduro, all point toward a more politically divided world and one where the U.S. dollar appears less appealing to many foreign governments as a reserve asset.

While there are good reasons for this sector to continue its outperformance, the prices of underlying commodity prices are beginning to look quite stretched, which is the nice way to say quite bubbly. A reversal in metals prices could present a headwind for metals and mining stocks although many mining companies have not fully adjusted to current metals prices anyway. Some companies could continue to see additional upside even if metals prices reverse their more recent gains, as existing mines are expanded and/or new mines are built to take advantage of historically high metals prices.

Performance of SPDR Gold Shares Trust (GLD, Light Blue) and iShares Silver Trust (SLV, Green)

10 Year Chart - January 1, 2016 to December 31, 2025

What’s Tech and AI Up To?

In line with much of the last 2-3 years, the distribution of returns within the technology sector was abnormally broad with Alphabet and Nvidia returning 65% and 39% year-to-date, respectively, while the average return of the remaining 5 Magnificent Seven stocks (Microsoft, Apple, Amazon, Meta, and Tesla) was ~11%. The Magnificent Seven may soon evolve into the Exceptional Eight following Broadcom’s 51% return in 2025, making it now the sixth largest company in the US by market cap. The distribution of returns of technology stocks in 2025 reflected unexpected AI advancements by Alphabet (which also boosted Broadcom’s outlook as an Alphabet partner in chip manufacturing), a growing and more confident chip sales pipeline for Nvidia and a more realistic outlook for many other AI companies. In Q4, investors began to scrutinize the future losses that are expected to be incurred by AI software companies (e.g. OpenAI projects it will lose $115 billion before turning a profit in 2030) and how this might affect the earnings and cash flow of their backers (e.g. Microsoft owns ~27% of OpenAI and is on the hook for 27% of those losses if it wants to maintain its ownership).

Performance of Alphabet (GOOG, Light Blue), Broadcom (AVGO, Dark Blue), Nvidia (NVDA, Green), Microsoft (MSFT, Red), Apple (AAPL, Orange), Meta (META, Cyan), Amazon (AMZN, Purple), and Tesla (TSLA, Gold)

January 1, 2025 to December 31, 2025

And The Economy?

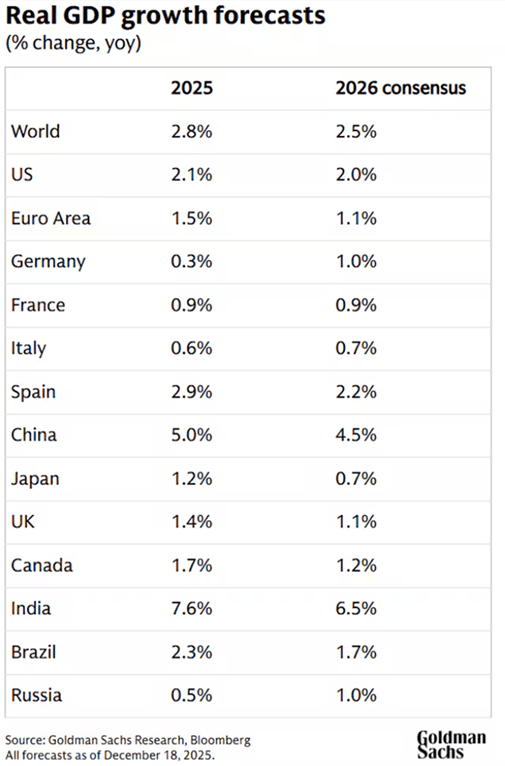

Global GDP growth remained subdued in 2025 as higher tariffs and ongoing trade uncertainty continues to hinder long-term investment, although worst fears about what tariffs might do to global trade were largely avoided. Expectations are that global GDP growth will continue to decline from current levels in 2026 and that those countries that suffered the most from trade disputes in 2025 will experience a rebound while most other nations will continue to feel the weight of tighter household and corporate budgets and gradually rising unemployment. The US economy is expected to outperform other developed nations once again in 2026 as continued investment in AI should continue to support capital investment and median wages in the US. Recent increases in metals prices could incite higher than expected growth in places like Canada, Brazil, Australia and Russia although capital investment in the metals and mining sector often comes with a notable lag so the benefits provided by higher commodity prices may be more visible in 2027 and beyond.

Despite lower-than-expected inflation figures in Q4, low but stable GDP growth and better than expected labour market data put interest cuts on pause in North America as the year wrapped up. As we noted last quarter, falling interest rates are unlikely to ignite significantly more investment in AI but they could incite additional investment in metals and mining investment as well as investment across many more traditional business sectors. Falling interest rates could further push investors toward economies dominated by commodities, housing and industrials like Canada and other non-US markets, but stable or even rising interest rates may cause investors to pivot back toward US AI and technology stocks which are less dependent on interest rate policy.

How To Position Portfolios Going Forward?

The AI investment cycle is sure to continue but AI/technology companies may have officially handed the stock market leadership baton to the metals and mining sector in 2025.

Greater Investment ≠ Higher Stock Prices

As we said last quarter, “the AI spending spree may be at the expense of lower earnings growth for U.S. megacap tech and potentially lower valuations for these companies over time”. Investors took this to heart very quickly and those companies with the largest future AI spending bills (e.g. Microsoft, Meta, Oracle) all struggled in Q4 while companies with minimal AI spending obligations (e.g. Alphabet) outperformed significantly.

Interest rate uncertainty could throw a wrench in what was a fairly smooth and ultimately definitive transition from big tech to metals and mining throughout 2025 but it is rare to see such a shift in market leadership and for that shift to not carry through for some time. We think this transition is likely to continue. This is positive for Canada, international markets, small- and mid-cap stocks, both in the US and abroad, and lower valuation stocks relative to higher valuation stocks. Sector wise, those sectors that benefit from broadening economic growth beyond just the technology sector – consumer discretionary, financials, industrials – could also continue to outperform in 2026 and beyond. Maintaining some exposure to big tech and AI is important given their large weighting in the global investment universe, but now that we’ve started to see obvious differentiation between big tech companies, being pickier about what you own could make a big difference going forward.

2025 was the first year in many where a truly diversified portfolio – across sectors, geographies and market caps – resulted in outperformance relative to the global equity benchmark which has a ~65% weighting to US equities, half of which is large cap technology companies. The rotation out of US technology stocks and into the rest of the investment universe appears to have significant momentum behind it, and if the start of trading in 2026 is any indication, this momentum is accelerating. Well diversified portfolios may prove to be the best way to participate in equity market upside for the foreseeable future.

Canadian perpetual and split corp preferred shares are attractive tax-efficient fixed income alternatives providing dividend yields of 5%-6% and should benefit from falling Canadian interest rates. While interest rate cuts appear to be on hold for now, the odds still favour interest rate cuts over hikes throughout 2026.

Alternative investments as a group continue to generate consistent yields with limited volatility.

Maintaining a well-diversified portfolio tailored to your risk tolerance is the best way to avoid major negative surprises and participate, if not capture the majority of upside provided by asset markets over time. You can be sure that we are tracking all market developments and are making portfolio adjustments to manage risk and pursue returns as investment opportunities arise.

If you ever have any questions or concerns about your portfolio or the investment markets in general, please feel free to reach out to us.

Sincerely,

|

|

|

|

|

|

|

|

|

|

|

The information contained in this report was obtained from sources believed to be reliable, however, we cannot present that it is accurate or complete. Information has been sourced from the RJL Bond Desk or RJ Private Client Solutions, unless otherwise noted. Index and sector returns represented in this commentary are measured using the S&P/TSX Total Return Index and S&P/TSX GICS Sector Indices as detailed in Raymond James Ltd.’s Insights & Strategies: Quarterly Edition. This report is provided as a general source of information and should not be considered personal investment advice or solicitation to buy or sell securities. The views expressed are those of the author and not necessarily those of Raymond James Ltd. (Member Canadian Investor Protection Fund).

This Quarterly Market Comment has been prepared by Steele Wealth Management and expresses the opinions of the author and not necessarily those of Raymond James Ltd. (RJL). Statistics and factual data and other information are from sources RJL believes to be reliable but their accuracy cannot be guaranteed. The performance outlined in the report is net of fees. The client account performance may vary from the model portfolio due to several factors, including the timing of contributions and dates invested in model. The performance reported is that of the account that represents the model, not a composite. Performance calculation for the models may be different than the index used as a reference point. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. This Quarterly Market Comment is intended for distribution only in those jurisdictions where RJL and the author are registered. Securities-related products and services are offered through Raymond James Ltd.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Raymond James (USA) Ltd. advisors may only conduct business with residents of the states and/or jurisdictions in which they are properly registered. Raymond James (USA) Ltd. is a member of FINRA/SIPC.

![]()