Canadian Housing Market Update: How Is It Holding Up?

Canadian Housing Market Update: How is it holding up?

Canadian mortgage rates hit 16-year highs in recent months. The best five-year fixed rate mortgage available in Canada currently sits at 4.64%.

Historical Best Five-year Fixed Mortgage Rates

This 4.64% mortgage rate is still low, historically, but debt levels are well above historical averages as well. Last July, we highlighted that Canadian housing at the time (May 2023), assuming a 5.4% five-year fixed rate mortgage, was the most unaffordable in history except for an 18-month period in 1981-1982. Affordability has improved by ~12% since our July 2023 analysis due to lower mortgage rates, but housing is still very unaffordable on a historical basis.

If affordability is so bad, how is the housing market holding up?

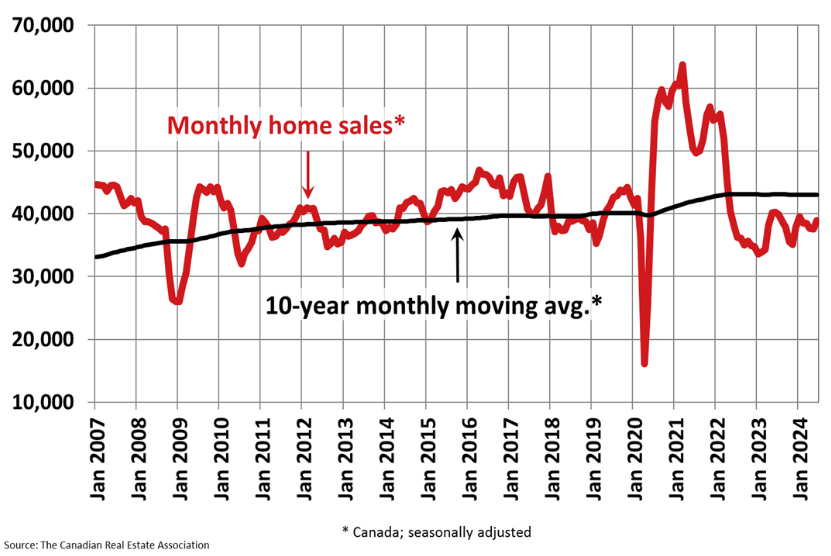

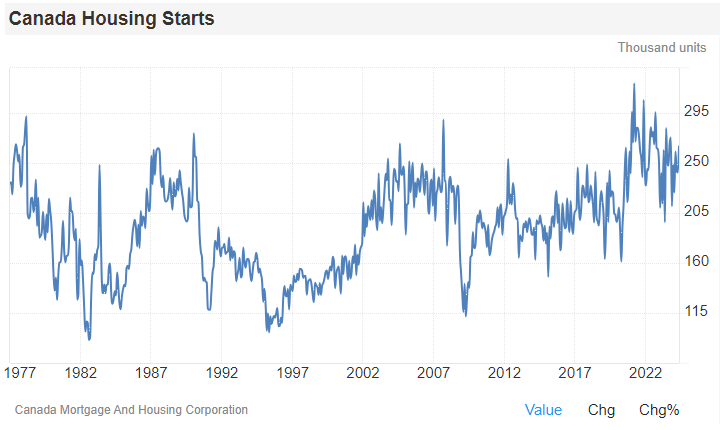

Pretty well, actually. Although Canadian monthly home sales (below) are lower than the 10-year monthly moving average, they remain at historically normal levels and the 10-year average is skewed by the high sales volumes during the pandemic period.

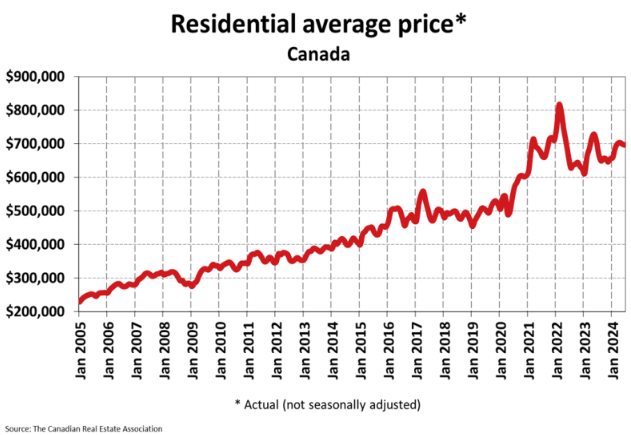

House prices remain well below the pandemic peak in early 2022 but continue to be quite resilient in the face of high interest rates and are generally trending higher following the price lows hit in early 2023.

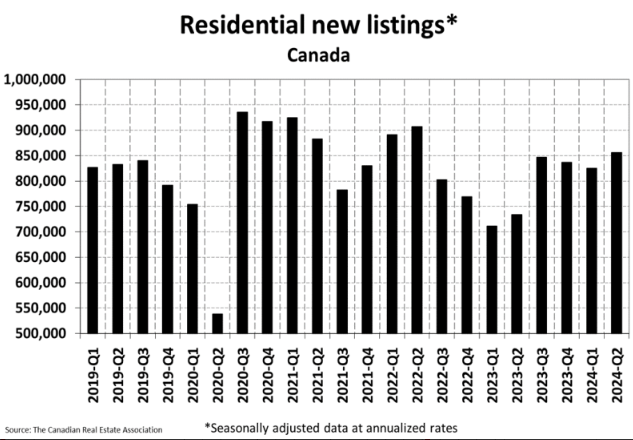

New listings are rising, up ~16% year-over-year in Q2 2024 but are near post-pandemic averages and are in line with pre-pandemic levels.

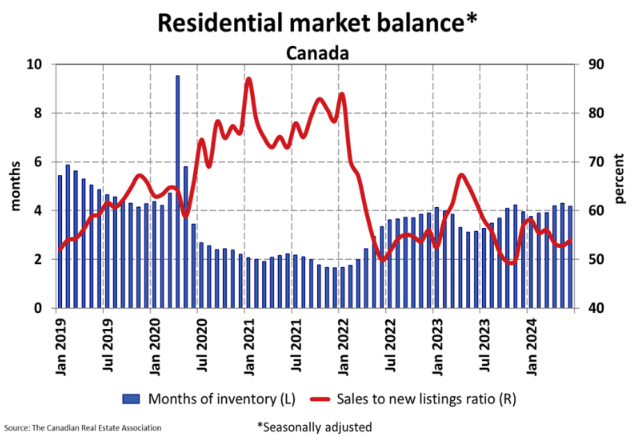

Months of inventory continue to sit at ~4%, below pre-pandemic levels, so the market continues to be somewhat supply-constrained, despite slightly-below-average home sales activity.

The pace of housing sales has stabilized, with selection near historically normal levels. Overall, the Canadian housing market appears to be well-balanced in the short term, though well-balanced doesn’t include those who are currently priced out of the market. Assuming no major changes, prices are likely to be fairly stable, going forward.

Changes to mortgage rates are the biggest wild card

If mortgage rates fall quickly, this could reignite demand for homes and we could revert to a bidding war type environment. After all, it is estimated that we will need to build 3.5 million or more houses by 2030 to improve affordability, and as of May 2024, the annualized building rate is 264,500. If the current construction rate continues, we will be 2 million or more homes short of what we need to improve affordability by 2030. Missing our housing construction target by that much would surely entrench an unaffordable housing market into Canadian society and this would have many negative consequences. Let’s get building!

If you’re ever looking to buy or sell your home, we can help develop a plan around this important life event including savings plans (for buyers), investment plans (for sellers) and guidance on how best to finance a property purchase. Feel free to reach out if you feel you’d benefit from our holistic insight.

News and our views

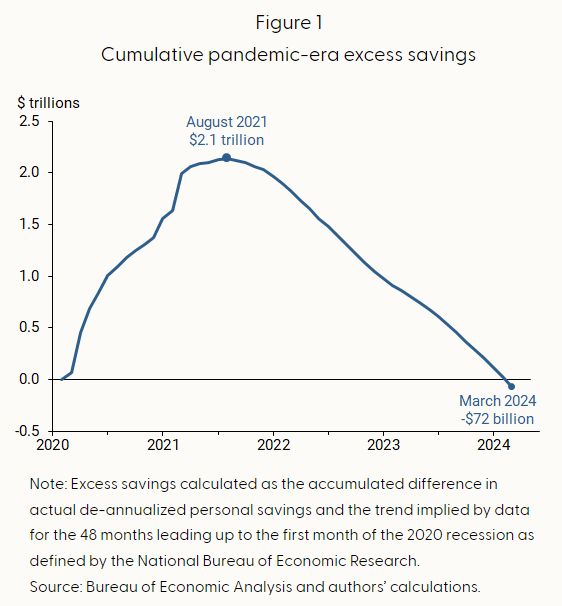

U.S. Consumers Are Tapped Out! In May 2024, the U.S. Bureau of Economic Analysis and the Federal Reserve Bank of San Francisco released estimates that all U.S. pandemic-era excess savings, which totalled as much as ~US$2.1 trillion in August 2021, have been depleted as of March 2024. This excess savings accumulated due to pandemic-related financial support to U.S. households and a decline in consumer spending related to social distancing and business closures in 2020 and 2021. After over two years of high and rising interest rates as well as high inflation not seen since the 1970s, consumers have had to spend through this excess savings and are now eating into savings that existed prior to the pandemic. Worse yet, U.S. consumers are taking on greater amounts of credit card debt, though on a positive note, delinquencies are still below pre-pandemic levels.

Our Take: U.S. consumers have been among the most resilient in recent years due to the overall strength of the U.S. economy and the lesser impact of interest rate hikes on U.S. consumers versus consumers outside of the U.S. U.S. consumers may begin to pull back spending more aggressively in the coming months, as excess pandemic-era savings are depleted and current spending rates mean that pre-pandemic savings are also being depleted. In recent months, we have seen large corporations including Nike, Starbucks, Dollar Tree, Home Depot, McDonald’s and PepsiCo ring the alarm bell on the struggling consumer, particularly the low- to middle-income consumer. The damage has been done for low-income households who are much more vulnerable to inflation and prices aren’t coming down anytime soon, although future inflation is hopefully now under control. Falling interest rates could help relieve the strain on the budgets of middle- and high-income households but it will likely take several more rate cuts and the passing of time before these consumers feel ready and able to spend again.

A Blowout Victory for the U.K.’s Labour Party and the Left-Wing Coalition Upsets France’s Rising Right. U.K. Labour leader Keir Starmer and party won 411 out of 650 seats, 211 more seats than the previous election. The Brits have provided the Labour party with a strong majority mandate, following 14 years of Conservative rule. Labour’s top priorities include new taxes on high-income households and energy companies, and greater spending on green investment, health care and schooling. In the second round of voting in France, the newly-formed coalition of left-wing parties (New Popular Front) teamed up with Macron’s incumbent centre-left coalition (Ensemble) to withdraw candidates in over 221 tight races to prevent vote splitting between left and centre-left candidates. As a result of this maneuvering, the right-wing National Rally garnered 37% of the vote, versus 26% for the second place New Popular Front, but only captured 25% of the seats.

Our Take: We expect very little change in both the U.K. and France following these elections. U.K. Labour’s policies are minor tweaks and should not materially affect investment in the U.K. nor are the proposed taxes overly onerous. In France, the party that won the most seats, left-wing New Popular Front, assumedly will have a minority government supported by Macron’s centre-left Ensemble, but at this point, a government has yet to be formed. Between the two coalitions, there are 13 individual political parties with very different views. So, governing the country may become difficult due to political infighting, and this could have negative economic consequences. Any political dysfunction in this new government may further bolster support for the right-wing National Assembly. Time will tell.

Just for fun

- McDonald’s is discontinuing the use of AI in U.S. drive-throughs. Since 2019, the company has been testing AI for order-taking in over 100 restaurants across the U.S., but due to unreliable results, the AI systems will be removed. Unreliable results include mistakenly massive chicken nugget orders, butter in place of caramel ice cream and bacon added to ice cream, which don’t sound all that bad really, especially the last one. The bare minimum requirement for AI should be to take fast food orders correctly, a function that is often a teenager’s first job. Until AI can compete with highschoolers, its impact in our society is likely to be minimal.

- You grill a burger, top with fresh-ish ingredients and reach for a sauce; what’s it going to be? Mustard, ketchup, mayo? Maybe you’re on to the new-age combo sauces like hanch (hot sauce and ranch) or mayochup (mayo and ketchup) or wasabioli (wasabi and aioli). How about a sauce that allows you to eat every sauce imaginable all at the same time? Our friends across the pond can now live this particular dream with Heinz’s new ‘Every Sauce.’ The mad scientists at Heinz U.K. have had enough with the two ingredient/sauce combinations and decided to throw all they had in the pot, combining 14 Heinz sauces into one. Perhaps we North Americans will be lucky enough to have our own Frankenstein of a sauce someday.

![]()