Reorganizing debt so that interest is tax deductible as an alternative to selling assets to cover debts

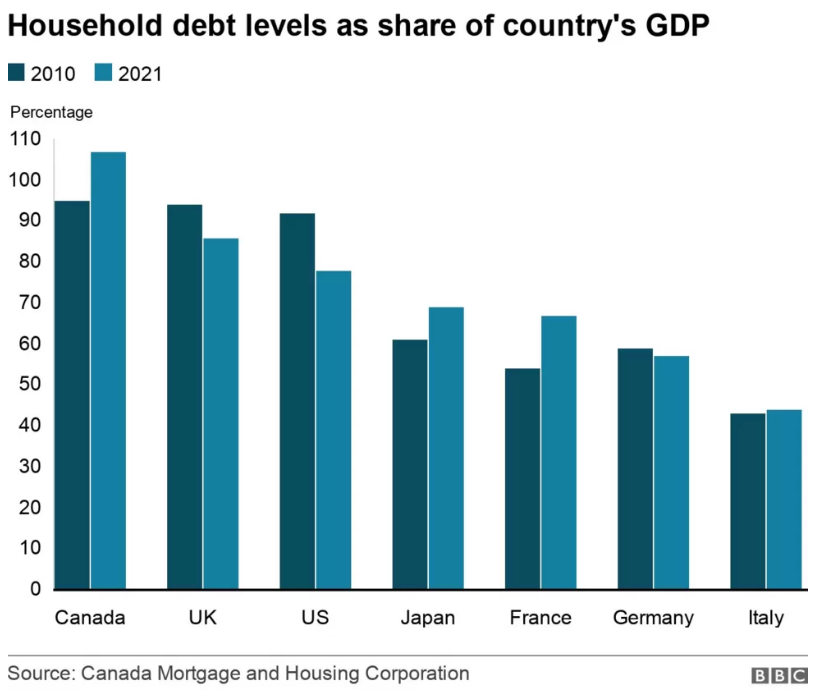

It is no secret that household debt in Canada is elevated. Canadian household debt levels as a share of GDP surpassed 100 per cent in 2021, and Canada now has the highest household debt relative to GDP of any G7 country, and by a wide margin.

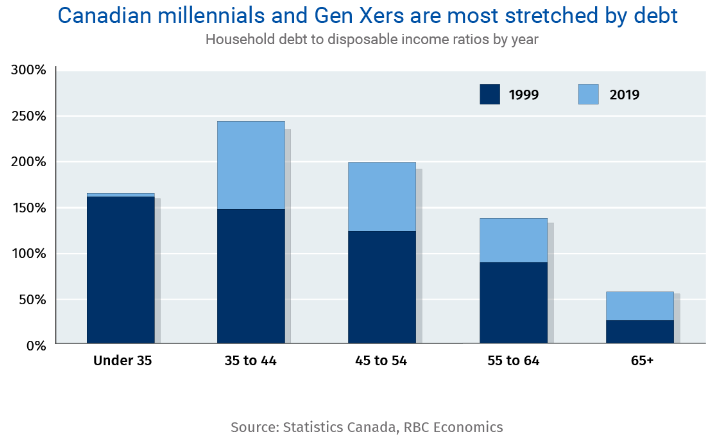

High house prices are the primary reason for elevated debt levels. Roughly, 75 per cent of Canadian household debt comes from mortgages backed by real estate. Intuitively, those at peak house buying age (i.e., first-time buyers and move-up buyers between age 35 and 54) carry far more debt relative to income than other age groups.

When interest rates are falling, servicing these high debt levels becomes easier over time. When interest rates are rising, servicing high debt levels can be difficult, if not impossible for some households. Mortgage rates have risen from under two per cent in 2021 to 5-7 per cent now, depending on the type of mortgage. As we noted in a previous blog post, 5-7 per cent mortgage rates on todays’ debt levels are similar to the financial stress that homeowners felt in the early 80s when mortgage rates were ~20 per cent but on much lower debt levels. For households with hundreds of thousands in mortgage debt, this 3%+ shift in interest rates will eat into discretionary income. The effect is immediate for those with variable rate mortgage debt or upon renewal for those with fixed rate mortgage debt, so not every household faces the same dilemma at the same time. One thing is for sure, higher interest/mortgage rates are coming for all of us borrowers, at some point, if mortgage/interest rates remain near current levels.

Liquidating an Investment Portfolio to Pay Down Debt

As interest rates rise, the natural reaction of many variable rate borrowers is to raise cash, from investments or otherwise, to pay down debt. Fixed rate borrowers often feel a similar urge as their renewal date(s), and higher mortgage rates, approach. Selling liquid assets like investments held in your non-registered accounts or TFSAs, which have less certain return expectations than the certain cost associated with a 5-7 per cent mortgage, can be appealing to many.

We agree that many fixed income securities and even some equities may have a difficult time outperforming a return hurdle of 5-7 per cent, especially if the investments are held in a non-registered account and investment income is subject to taxation. Liquidating these types of investments to pay down debt may make sense. Doing so is a way to de-risk your finances at a time of high financial stress. You are effectively selling riskier and potentially lower return-generating fixed income and equity investments and “buying” your low-risk mortgage that pays 5-7 per cent.

Restructuring Debt So That Mortgage Interest Costs Are Tax Deductible

Generally, mortgage interest on an owner-occupied home is not tax deductible in Canada. One strategy, to convert non-deductible mortgage interest into interest that may be deductible, is to repay the existing mortgage and reborrow to invest the proceeds. The steps in the strategy are to liquidate a non-registered investment portfolio, pay off the initial mortgage, initiate a new mortgage and invest the mortgage proceeds in a non-registered investment portfolio. If the repurchased investment portfolio generates investment income, the mortgage interest may be tax deductible, subject to some conditions. It is important to note that you must not use new borrowed funds to pay off the old/original mortgage or else the interest will not be tax-deductible. The flow of funds must be traceable and is an important step in this process to ensure tax-deductibility.

Mortgage interest could also be tax deductible for those who opt to invest the proceeds of a home equity line of credit (HELOC) in an investment portfolio. While this strategy is certainly not for the risk averse, it allows you to maintain exposure to investment markets while attaining a tax deduction of mortgage interest.

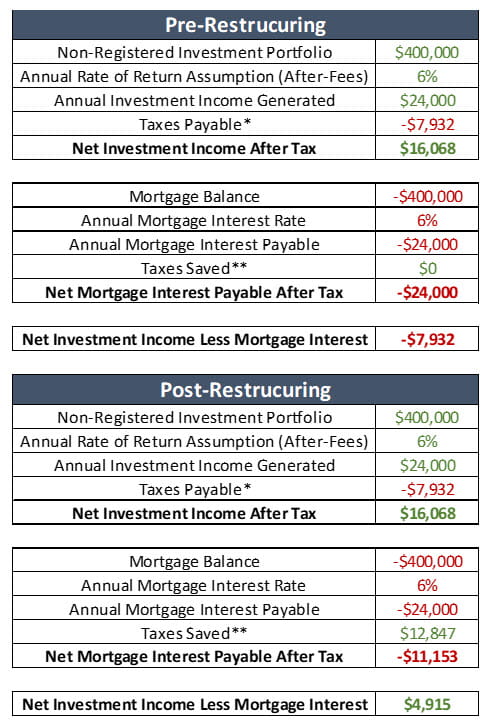

Below is an example of how restructuring your debt to make mortgage interest tax deductible helps the bottom line:

*Assumes highest marginal tax rate and 100 per cent Canadian dividend income

**Assumes highest marginal tax rate and interest is deductible from income

Assuming a six per cent annual after-fee rate of return on investments in a non-registered portfolio, all investment income generated being Canadian dividend income in the non-registered portfolio, and an annual mortgage rate of six per cent, a taxpayer who is at the top marginal tax rate and has $400,000 in mortgage debt would experience an annual net benefit of ~$12,847 by restructuring his or her debt to be tax deductible.

This strategy may not be feasible if the investment portfolio liquidated to pay off the old mortgage has sizable capital gains associated. The gains realized on liquidation would be taxable and the tax payable may be too significant to make this strategy practicable. As well, to avoid the superficial loss rules, any investments sold at a loss should not be repurchased within 30 days. Another notable point is that any interest payable on funds borrowed to invest in a Tax-Free Savings Account (TFSA), or any other tax-deferred account (RRSP, RESP, etc.), is not tax-deductible.

There are other specific requirements to ensure that mortgage interest is tax deductible:

- The money borrowed must be used for the purpose of earning income (e.g., interest, dividend, rents and royalties). If there is no expectation of earning these types of investment income, then the interest may not be tax deductible (i.e., the expectation of capital gains alone is not enough).

- You must pay the interest owing on the mortgage loan in the year you claim the deduction.

- There must be a legal obligation to pay the interest (i.e., it cannot be an ad hoc mortgage provided by a family member or close friend).

- The interest charged must be reasonable (i.e., the interest rate must be close to market rates).

While liquidating your investment portfolio to pay off a potentially high interest mortgage can make sense in many cases, it is worth reviewing if restructuring your debt so that interest is tax deductible is advantageous in your situation.

If you have a variable rate mortgage or a mortgage renewal coming up, we are happy to review your options with you.

News and our views

Canadian Economy Shrinks in Q2, Re-Sparking Recession Fears. Canada’s economy shrunk by 0.2 per cent on an annualized basis in the second quarter, missing Bank of Canada’s and analysts’ expectations of annualized growth of 1.5 per cent and 1.2 per cent, respectively. The GDP miss was driven by the fastest decline in housing investment since the 1980s, as new construction fell 8.2 per cent and renovation spending fell 4.3 per cent in the quarter.

Our Take: While the pace of the decline is surprising, the direction of housing investment is not. The rapid increase in interest and mortgage rates makes housing less affordable for households, but it also deters property developers from building new properties. This will only further worsen the supply-demand imbalance in the Canadian housing market and boost long-term pent-up demand for housing. We expect falling housing investment to continue to drag on the Canadian economy in the coming quarters if interest and mortgage rates remain near current levels. However, an eventual reduction in interest and mortgage rates, and a subsequent rebound in housing investment, will likely be a primary driver of strength in the Canadian economy in the coming years. An annualized GDP decline of 0.2 per cent is about as soft landing as you can get, and considering the quarter’s weakness was driven by the economic impact of high interest rates, which are at the Bank of Canada’s discretion, a soft landing is still very much a possibility. In recent days, Ontario Premier Doug Ford and B.C. Premier David Eby have pleaded to the Bank of Canada to halt interest rate hikes, a sign that economic weakness is putting political pressure on the Bank.

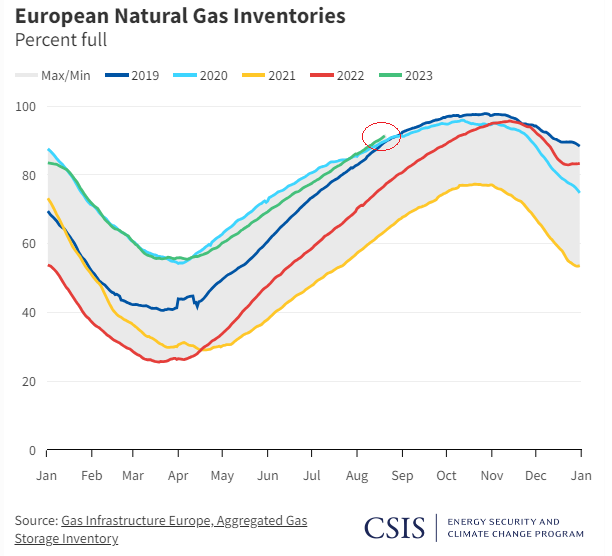

European Gas in Storage a Good Sign for Future EU Inflation. The EU reached its 90 per cent gas storage target roughly two-and-a-half months ahead of its own November 1 deadline. While all four-season nations/continents seasonally build up natural gas reserves from spring to fall and draw those reserves from fall to spring, the EU is much more reliant on its reserves due to little natural gas production of its own. In the fall of 2022, the EU was scrambling to fill its natural gas storage facilities, paying more than 10x the current natural gas price to shore up its natural gas storage as it faced potential supply shortages resulting from the war in Ukraine and worsening relations with its #1 source of natural gas, Russia. Paying so much to fill its natural gas facilities was a major factor in driving EU inflation in late 2022 and early 2023. The winter temperatures experienced in the EU ended up being the mildest in decades, and the continent avoided natural gas shortages and disruptions to industrial activity. But it still had to suffer the inflation caused by the high cost of natural gas purchased to prepare for winter.

Our Take: Achieving the 90 per cent gas storage target early reduces the odds that the EU will experience an energy crisis as it did in 2022, albeit the energy crisis was not as bad as it could have been. Building up inventories when natural gas prices were reasonable means that future energy price inflation should be limited in the EU over the next six to nine months. The potentially disastrous EU energy crisis in 2022 could have had far-reaching impacts on global growth and inflation. Much lower odds of the EU facing such a crisis and negligeable energy inflation in the EU are good for global growth and the global fight against high inflation.

Just for fun

- August marked the largest search for the Loch Ness Monster in 50 years with hundreds of Nessie enthusiasts making the trip to Loch Ness to look out for the prehistoric beast, and they found it! Just kidding. Nessie may never be found, but it will surely live in the imaginations of many for centuries.

- Hank the Tank, the World’s Most Infamous Bear. The bear, also known as Bear 64F, was captured in early August and is accused of at least 21 cases of breaking and entering. Hank could be part of a syndicate of “conflict bears” suspected to have caused 152 reports of conflict behaviour in South Lake Tahoe, California. Though “conflict bears” sounds intense, by all measures, Yogi Bear would qualify as a conflict bear given his larcenist ways.

- The Women’s World Cup semifinal match between Australia and England broke broadcast records in Australia with 11.5 million viewers tuning into the match. That equates to 43 per cent of the entire population of Australia! What a great day for Australian national pride and a testament to the growing draw of women’s professional sports.

![]()